Resolving the Defined Benefit vs. Defined Contribution Dilemma

You've been told it's either maximizing your personal wealth or providing affordable benefits to your team. It's actually neither.

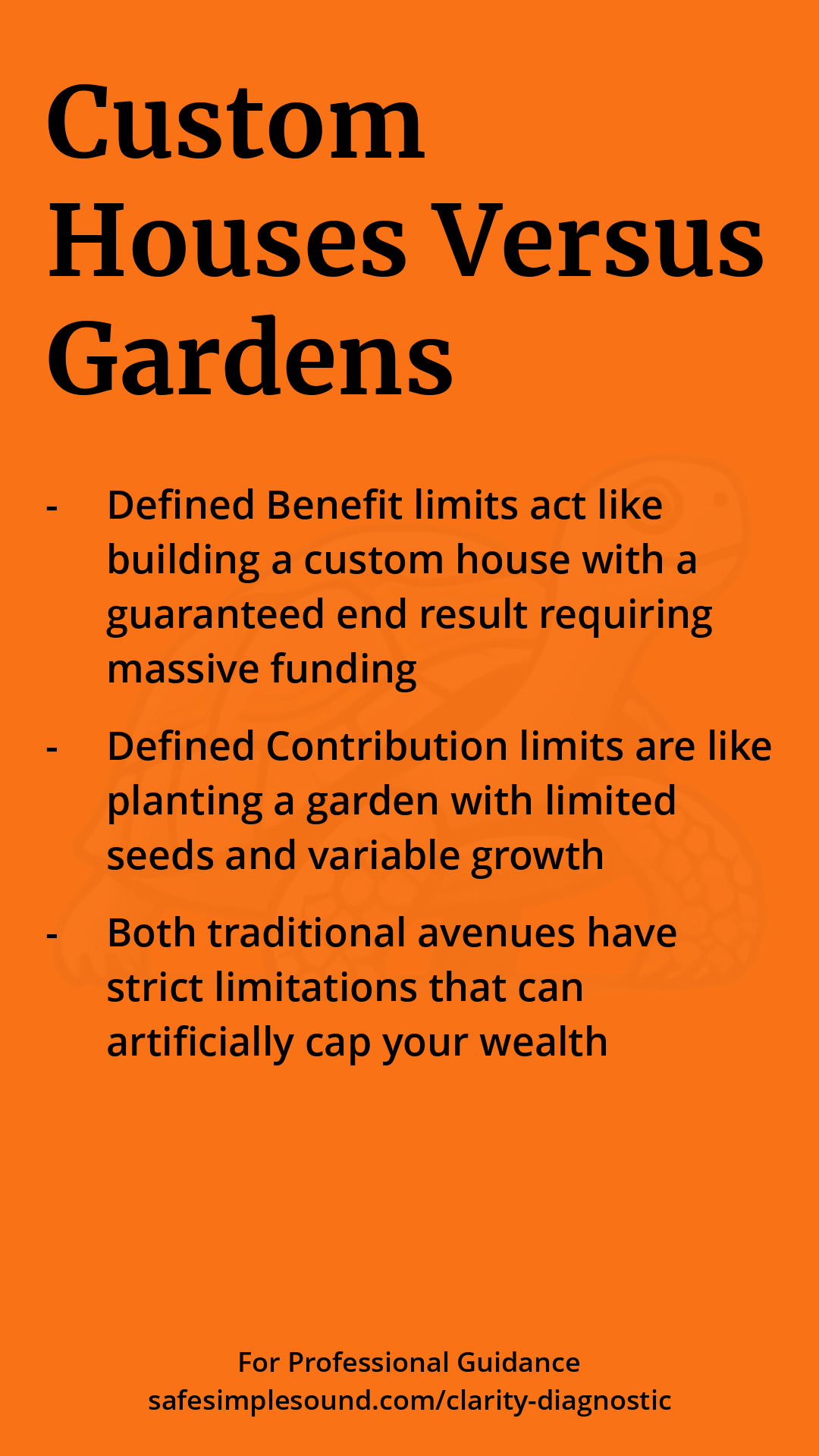

Traditional financial narratives force high-income earners into a false choice. They dictate that you must sacrifice your own retirement architecture to care for your employees.

There is a hybrid structure that solves this wealth versus benefits contradiction.

A few things worth knowing before you accept a standard broker's quote:

→ Defined Benefit plans act like building a custom house—they guarantee an end result but require massive, inflexible funding.

→ Defined Contribution plans are like planting a garden—growth is variable and your personal wealth accumulation is artificially capped.

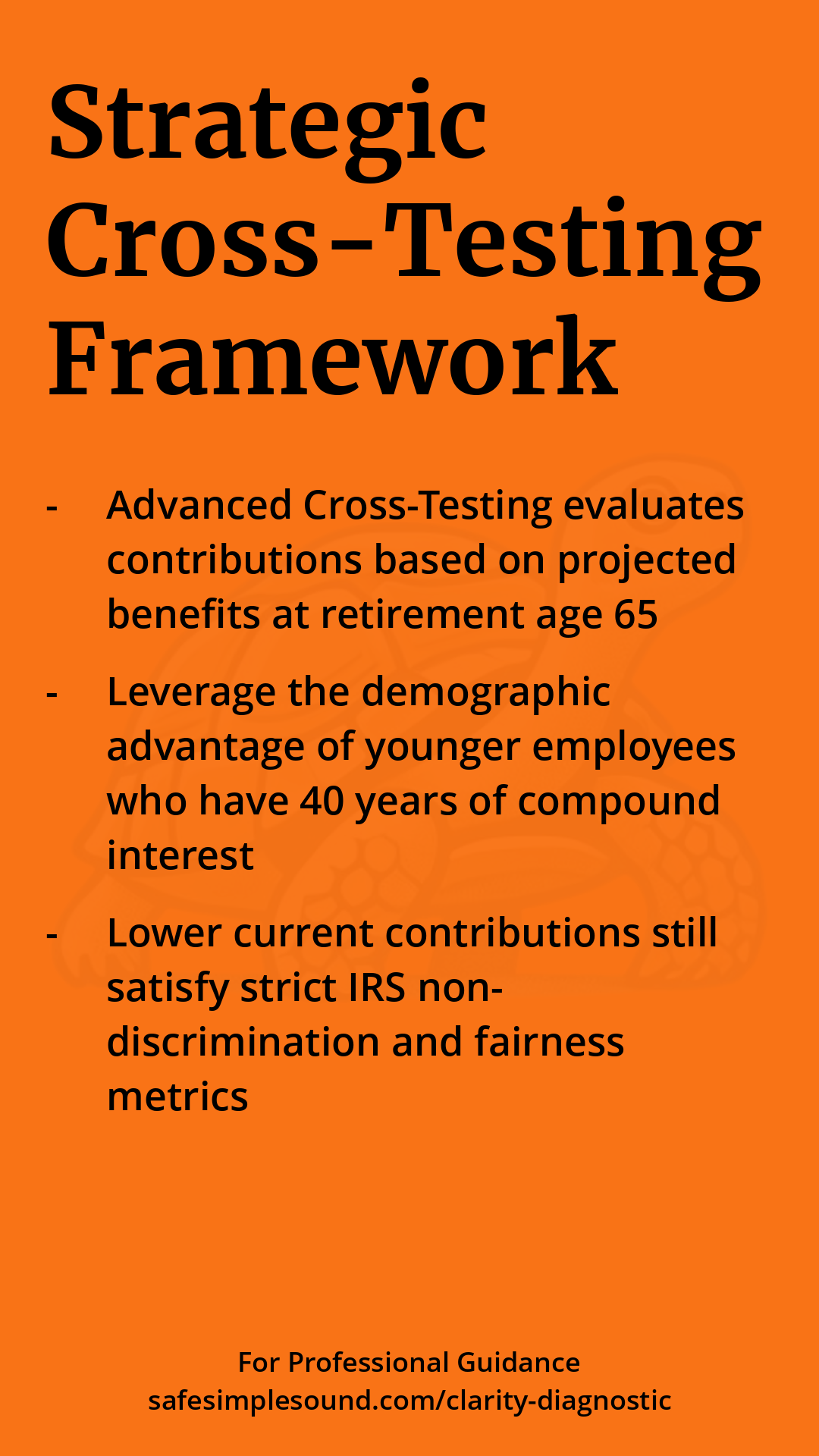

→ The Cash Balance Plan bridges the gap. It operates as a high-limit Defined Benefit plan for the owner, but looks like a simple account balance to the employee.

→ The math is staggering. By using advanced cross-testing, two 55-year-old owners can legally sheltered $400,000 for themselves while spending just $35,000 on their team—bypassing an unaffordable $150,000 quote from standard brokers.

I put the full breakdown below.

If you want to understand the actuarial math or audit your own demographic profile, the full episode is available at SafeSimpleSound.com.

DISCLAIMER: This content is for educational purposes only and should not be considered personalized financial advice. Always consult with a qualified financial professional before making financial decisions.